Explore our network of country and industry based websites to access localized information, product offerings, and business services across our group.

Log in to start sending quotation requests for any product.

Don't have an account? Sign Up Here

Home Global Citrus Pulp Supply Chain Outlook 2026: Trade, Pricing and Logistics

Trade Insights | Supply Chain | 27 April 2026

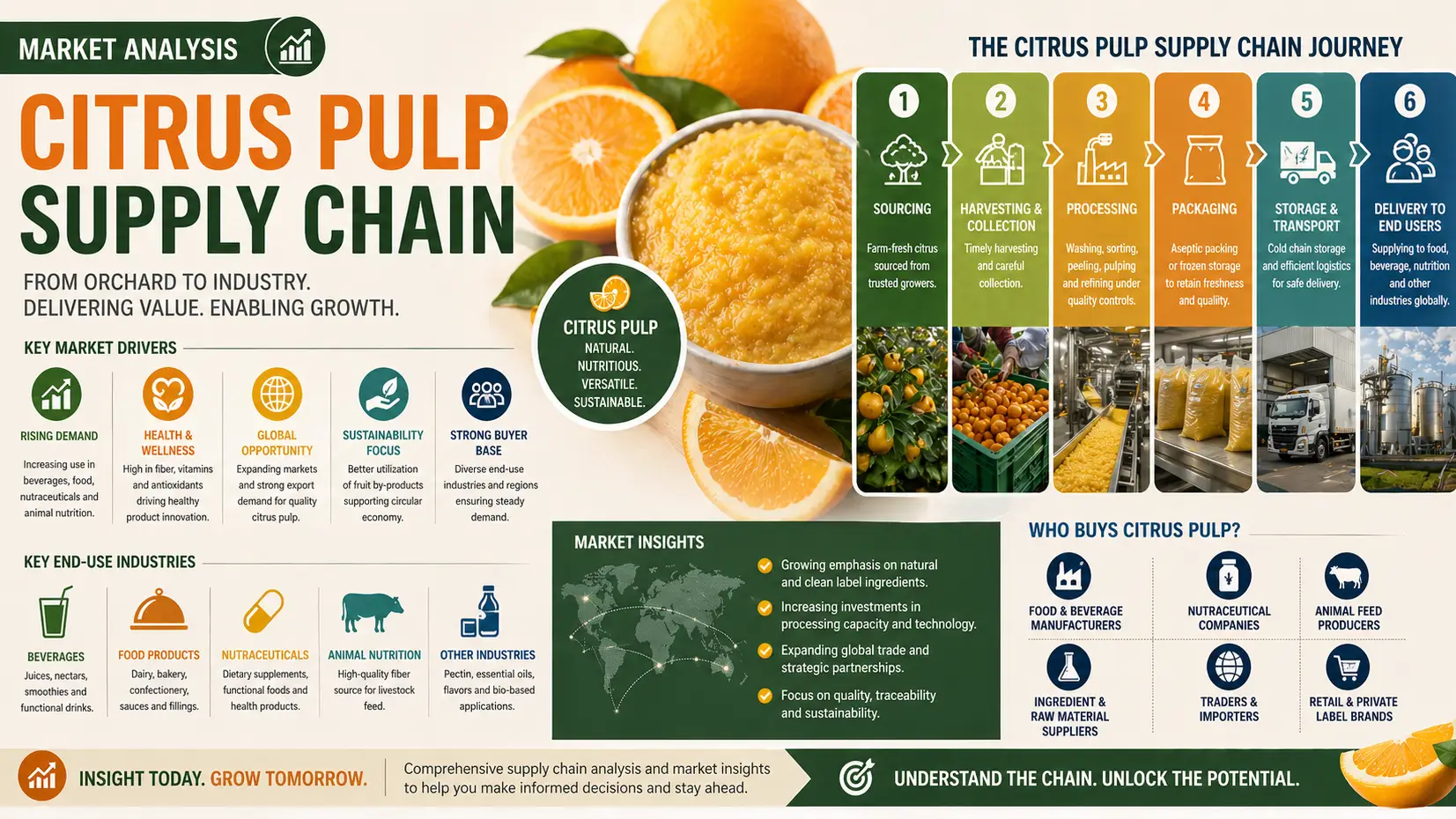

Citrus pulp, widely recognized as a valuable byproduct of citrus juice processing, is increasingly positioned in 2026 as a platform feed ingredient supporting circular bioeconomy models across global agribusiness. As supply chains mature, producers and traders are navigating shifting availability from major citrus-growing regions, while balancing cost efficiency and sustainability expectations. The market demonstrates steady expansion, with a projected CAGR of 4.8%, driven by livestock feed demand, price competitiveness, and rising utilization of processed agricultural residues.

Citrus pulp supply chains in 2026 remain highly fragmented, with processing hubs concentrated in Brazil, the United States, and Spain. Seasonal juice production generates uneven output, contributing to volatility in dried pulp availability. Global production is estimated at 5.2 million MT, creating logistical imbalances between surplus and deficit regions. This fragmentation increases dependency on intermediaries who aggregate wet pulp before dehydration and export across global trade corridors.

Demand from livestock feed manufacturers remains the primary growth driver, as citrus pulp offers digestible fiber and energy content at competitive pricing. In 2026, average market prices range between USD 120–180/MT, reflecting feed-grade quality differentials and moisture reduction costs. Price transmission is heavily influenced by corn and soybean meal volatility, reinforcing citrus pulp’s role as a cost stabilizer in compound feed formulations across poultry and dairy sectors globally.

Logistics efficiency remains a decisive factor in citrus pulp trade, as wet pulp requires rapid processing to prevent spoilage. Advances in rotary drum drying and pelletizing technologies have improved shelf life and reduced transportation costs per ton-mile. Cold-chain integration is limited, so producers rely on regional dehydration plants. These improvements support stable export flows and reduce post-harvest losses across major supply corridors.

International trade flows are increasingly shaped by sustainability mandates, with citrus pulp valorized as a circular economy input in feed and bio-based applications. Exporters in Latin America and Europe are optimizing certification and traceability systems to meet buyer requirements. Demand for non-GMO and low-residue feedstock is expanding, reinforcing premium segmentation within the market and strengthening long-term contract structures particularly in Europe and Asia-Pacific feed markets driven by regulatory alignment.

Citrus pulp as a platform chemical continues to demonstrate strong relevance in diversified agro-industrial value chains, linking feed, sustainability, and trade efficiency. As supply chain resilience becomes a priority in 2026, market participants are increasingly seeking integrated sourcing and distribution partners. In this context, Tradeasia International offers a reliable global platform for procurement, logistics coordination, and supply continuity, enabling buyers to navigate price volatility and regional supply constraints effectively while securing consistent quality and volume access.

Sources

https://www.fao.org/agriculture/citrus/en/

https://www.usda.gov/

https://www.mordorintelligence.com/industry-reports/citrus-pulp-market

We're committed to your privacy. Tradeasia uses the information you provide to us to contact you about our relevant content, products, and services. For more information, check out our privacy policy.

English

English

Indonesian

Indonesian

简体字

简体字

العربية

العربية

Español

Español

Français

Français

Português

Português

日本語

日本語

한국어

한국어

Tiếng Việt

Tiếng Việt