Explore our network of country and industry based websites to access localized information, product offerings, and business services across our group.

Log in to start sending quotation requests for any product.

Don't have an account? Sign Up Here

Home Fish Meal Supply Chain Outlook 2026: Trade Flows, Prices & Production Trends

Trade Insights | Supply Chain | 23 April 2026

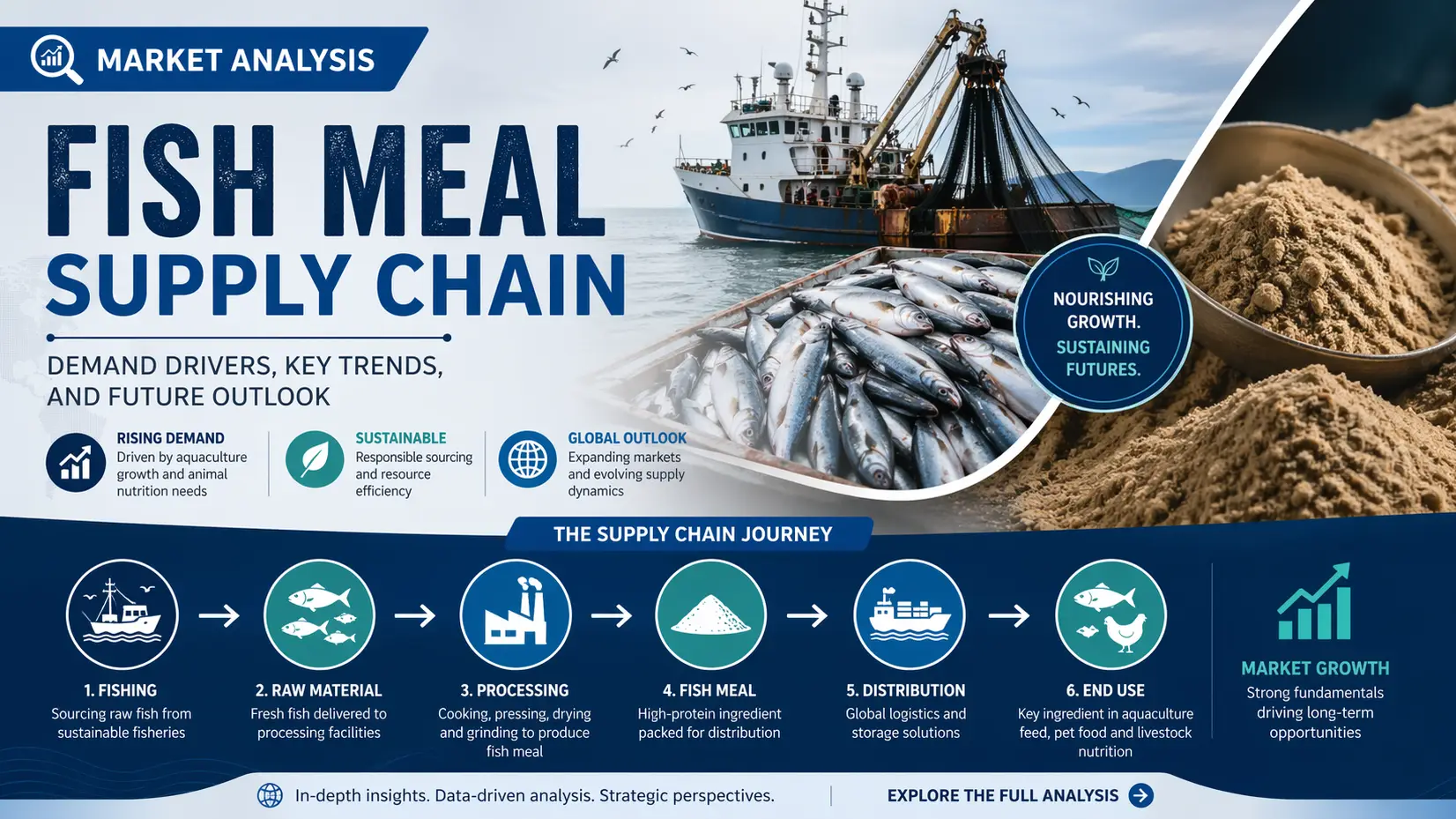

Fish meal continues to position itself as a critical platform feed ingredient within the global aquaculture and livestock nutrition ecosystem in 2026, driven by its high protein density and digestibility profile. As demand for sustainable aquafeed intensifies, the fish meal supply chain is undergoing structural recalibration, balancing resource constraints with industrial-scale processing efficiency. The global market is projected to grow at a moderate CAGR of 4.2%, supported by aquaculture expansion in Asia and Latin America. Average export pricing remains elevated at USD 1,650–1,950/MT, while global production volumes stabilize near 5.4 million metric tons annually, reflecting tight raw material availability.

The upstream segment of the supply chain remains heavily dependent on wild-caught pelagic fish, particularly anchovy fisheries in Peru and Chile, which collectively contribute over 35% of global fish meal output. Climate variability, including El Niño cycles, continues to disrupt catch volumes, causing supply volatility. In 2026, raw fish input costs have increased by nearly 12% year-on-year, tightening margins for processors and intensifying competition for certified sustainable fisheries.

Downstream processing infrastructure is increasingly concentrated in high-efficiency coastal hubs. Modern reduction plants operate at utilization rates exceeding 78%, yet energy costs and compliance with environmental standards are pushing production costs upward. Average cash production cost has risen to approximately USD 1,100–1,300/MT, forcing smaller mills out of the export chain. Vertical integration between fishing fleets and processors is becoming a defining competitive strategy.

Global trade flows remain highly regionalized, with Peru, Vietnam, and Denmark acting as key export nodes. Freight volatility and port congestion have added an additional 8–10% cost premium to landed fish meal prices in import-heavy regions such as China and the EU. Long-term contracts are increasingly preferred over spot trading, as buyers seek stability amid fluctuating availability and currency-driven price shifts.

Aquaculture feed manufacturers dominate demand, accounting for nearly 68% of total consumption, particularly within salmon, shrimp, and tilapia production systems. Feed formulators are gradually reducing fish meal inclusion rates, yet premium aquafeed segments still rely on its nutritional performance. This structural demand ensures sustained procurement even as alternative proteins expand.

As a platform protein ingredient, fish meal remains deeply embedded in global feed formulation strategies despite rising cost pressures and supply volatility. Its supply chain is becoming more consolidated, data-driven, and sustainability-focused, reflecting broader shifts in marine resource management. In this evolving landscape, global procurement partners such as Tradeasia International play a vital role in connecting reliable sourcing networks with industrial buyers, ensuring continuity, quality assurance, and optimized trade execution across fragmented markets.

Sources

We're committed to your privacy. Tradeasia uses the information you provide to us to contact you about our relevant content, products, and services. For more information, check out our privacy policy.

English

English

Indonesian

Indonesian

简体字

简体字

العربية

العربية

Español

Español

Français

Français

Português

Português

日本語

日本語

한국어

한국어

Tiếng Việt

Tiếng Việt