Explore our network of country and industry based websites to access localized information, product offerings, and business services across our group.

Log in to start sending quotation requests for any product.

Don't have an account? Sign Up Here

Home MBM Supply Chain Outlook 2026: Trade Flows, Pricing & Global Dynamics

Trade Insights | Supply Chain | 23 April 2026

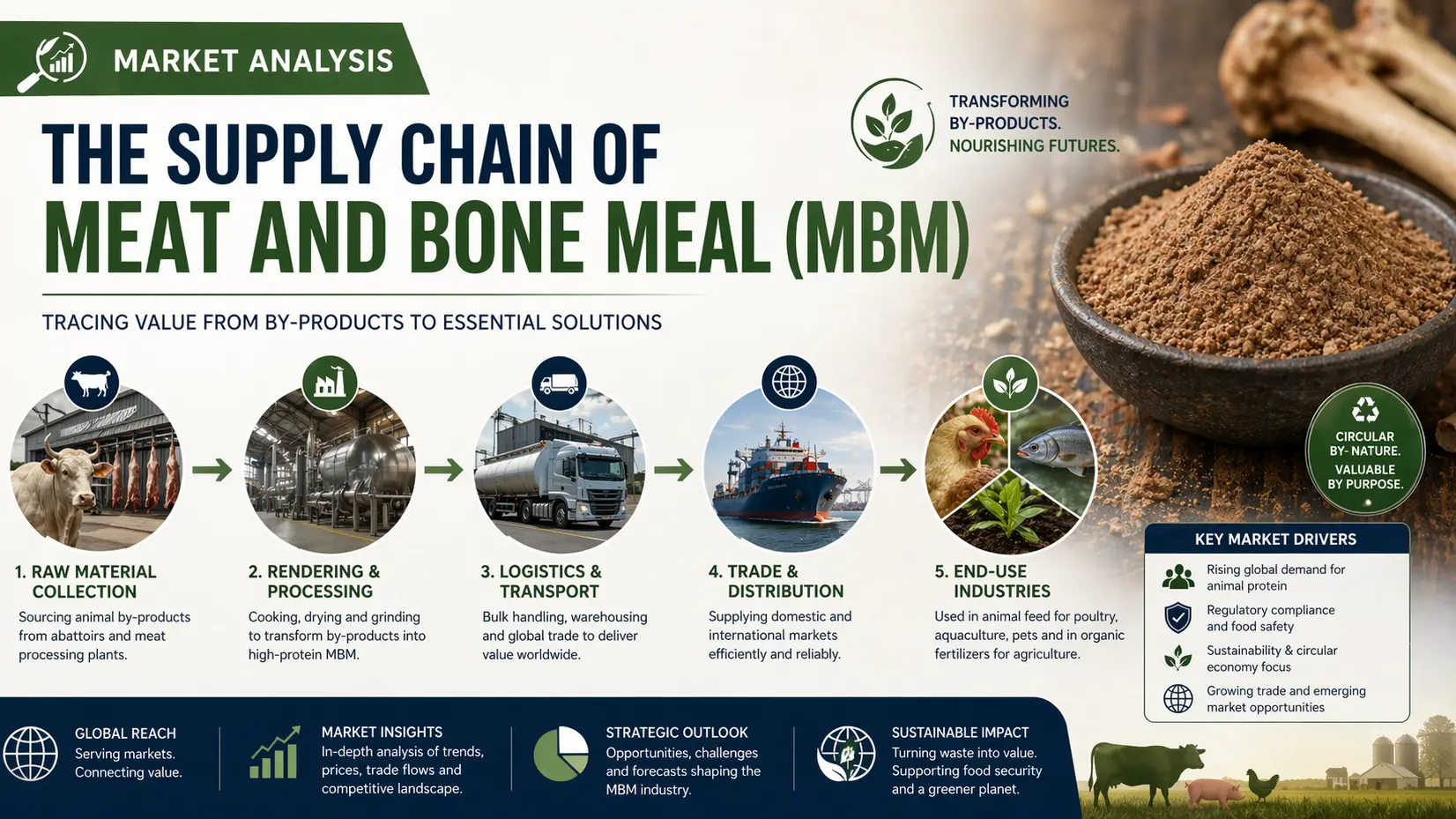

Meat and Bone Meal (MBM) continues to position itself as a critical platform ingredient in the global feed and agricultural value chain as of 2026. Derived from rendered animal by-products, MBM supports protein recycling systems in livestock, aquaculture, and pet food industries. The global MBM market is expanding at a steady 3.8% CAGR, driven by rising demand for cost-efficient protein alternatives. Market pricing has stabilized within USD 420–650/MT, while total production volumes are estimated at approximately 12.5 million metric tons annually, reflecting both regulatory constraints and rising rendering efficiency.

MBM production remains heavily concentrated in North America, Europe, and parts of Asia-Pacific, where integrated rendering infrastructure is mature. The United States alone accounts for nearly 3.1 million MT of annual output, while the EU contributes close to 2.4 million MT, driven by strict waste valorization policies. Emerging economies such as Brazil and India are increasing output capacity, but infrastructure gaps continue to limit scalability. This geographic imbalance is reshaping global sourcing strategies and encouraging import dependency in protein-deficit regions.

The feed sector remains the dominant consumer of MBM, absorbing more than 70% of global supply. Poultry and aquaculture feed formulations are increasingly integrating MBM as a cost-control protein substitute. Trade flows are intensifying between surplus producers and deficit regions in Southeast Asia and the Middle East. Export corridors from the EU to Vietnam and Indonesia have expanded significantly, while tariff adjustments in China continue to influence regional redistribution of nearly 4.8 million MT in annual trade volumes.

Although MBM does not require cold chain logistics, its supply chain is highly sensitive to biosecurity regulations and transport compliance. Rendering plants must adhere to stringent HACCP and EU animal by-product regulations, increasing operational costs by nearly 12–15%. Cross-border shipments are further complicated by veterinary certification requirements, especially in halal-compliant markets. These regulatory layers create friction in supply chain fluidity, particularly for exporters targeting high-growth Asian feed markets.

MBM pricing remains volatile due to fluctuations in livestock slaughter rates and rendering input availability. In 2026, average global prices range between USD 420–650/MT, with upward pressure from energy costs and compliance expenses. Margin compression is evident among mid-tier processors, while integrated rendering companies benefit from economies of scale. Futures-style procurement contracts are increasingly used to stabilize procurement costs across large feed manufacturers.

As sustainability reshapes global protein supply chains, MBM continues to function as a key platform chemical within circular feed systems, converting waste into value-added nutrition streams. Its role in reducing feed costs while supporting resource efficiency strengthens its long-term industrial relevance. Companies seeking to optimize procurement efficiency and ensure consistent MBM supply can benefit from integrated sourcing and global distribution expertise offered by Tradeasia International, a trusted partner in chemical and feed ingredient supply networks.

Sources

We're committed to your privacy. Tradeasia uses the information you provide to us to contact you about our relevant content, products, and services. For more information, check out our privacy policy.

English

English

Indonesian

Indonesian

简体字

简体字

العربية

العربية

Español

Español

Français

Français

Português

Português

日本語

日本語

한국어

한국어

Tiếng Việt

Tiếng Việt