Explore our network of country and industry based websites to access localized information, product offerings, and business services across our group.

Log in to start sending quotation requests for any product.

Don't have an account? Sign Up Here

Home Beet Pulp Supply Chain 2026: Global Trade, Logistics and Market Dynamics

Trade Insights | Supply Chain | 28 April 2026

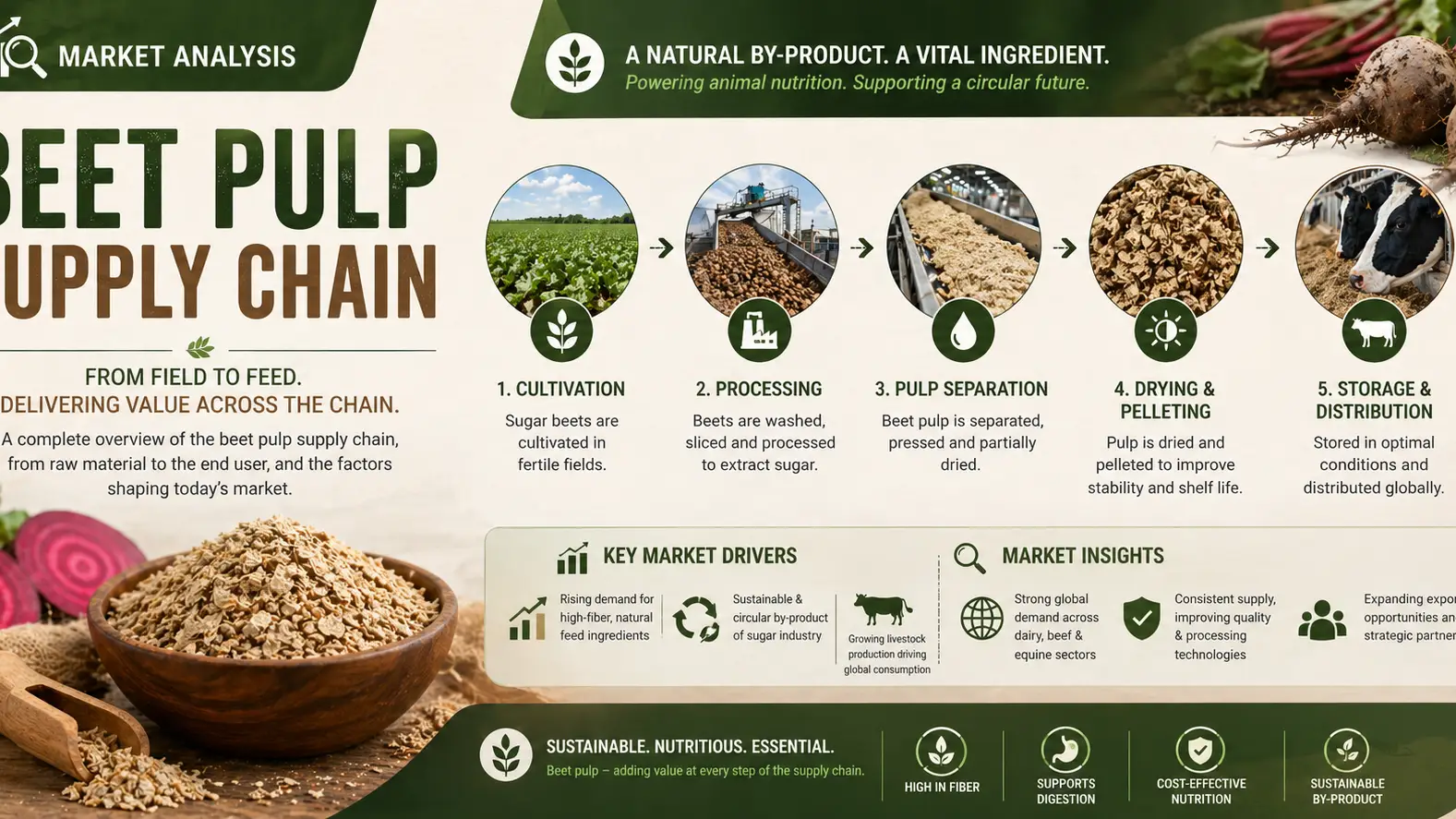

Beet pulp, a co-product derived from sugar beet processing, is increasingly positioned as a strategic platform bioproduct within the global agro-industrial ecosystem. In 2026, its supply chain reflects a mature yet evolving structure shaped by agricultural cycles, energy costs, and livestock feed demand. With a global market size exceeding 8.6 million metric tons, beet pulp continues to serve as a cost-efficient fiber source, trading at an average of USD 120–180/MT depending on moisture content and region. The market is projected to expand at a steady 4.8% CAGR, driven by rising demand for sustainable animal nutrition inputs.

The upstream supply of beet pulp is tightly linked to sugar beet cultivation in Europe, Russia, and North America. The EU alone contributes nearly 45% of global production, benefiting from integrated sugar processing facilities. Procurement efficiency is increasingly influenced by climate variability and beet yield fluctuations, which directly affect pulp availability and pricing stability.

Processing facilities are shifting toward dehydration and pelletization to extend shelf life and improve transport economics. Pelletized beet pulp commands a premium of USD 15–25/MT over wet pulp due to reduced logistics costs and enhanced feed formulation flexibility. Automation and energy-efficient drying systems are becoming critical to maintaining margins amid rising utility expenses.

The trade flow of beet pulp is highly export-oriented, with the EU and US supplying high volumes to Asia and the Middle East. Global export volumes are estimated at 3.2 million MT annually, with freight costs representing up to 20% of landed pricing. Port congestion and container availability continue to shape lead times, particularly in peak livestock feeding seasons.

Demand is concentrated in dairy and beef cattle industries, where beet pulp is valued for its digestible fiber content. Rapid growth in intensive dairy farming in Asia is reinforcing import dependency, especially in markets like China and Vietnam, where feed diversification strategies are accelerating.

As beet pulp strengthens its position as a reliable, sustainable feed ingredient within global agriculture, supply chain integration becomes a decisive factor for competitiveness. From procurement resilience to logistics optimization, stakeholders are increasingly seeking partners capable of ensuring continuity and quality assurance. In this context, Tradeasia International emerges as a trusted global solution provider, supporting seamless sourcing and distribution across diversified agro-commodity markets.

For companies navigating volatile feedstock markets, aligning with established trade intermediaries like Tradeasia International can significantly enhance supply chain efficiency, risk mitigation, and long-term procurement stability.

Sources

We're committed to your privacy. Tradeasia uses the information you provide to us to contact you about our relevant content, products, and services. For more information, check out our privacy policy.

English

English

Indonesian

Indonesian

简体字

简体字

العربية

العربية

Español

Español

Français

Français

Português

Português

日本語

日本語

한국어

한국어

Tiếng Việt

Tiếng Việt