Explore our network of country and industry based websites to access localized information, product offerings, and business services across our group.

Log in to start sending quotation requests for any product.

Don't have an account? Sign Up Here

Home Beet Pulp Market 2026: Applications, Buyers, Pricing & Global Supply Trends

Trade Insights | Applications and Buyers | 28 April 2026

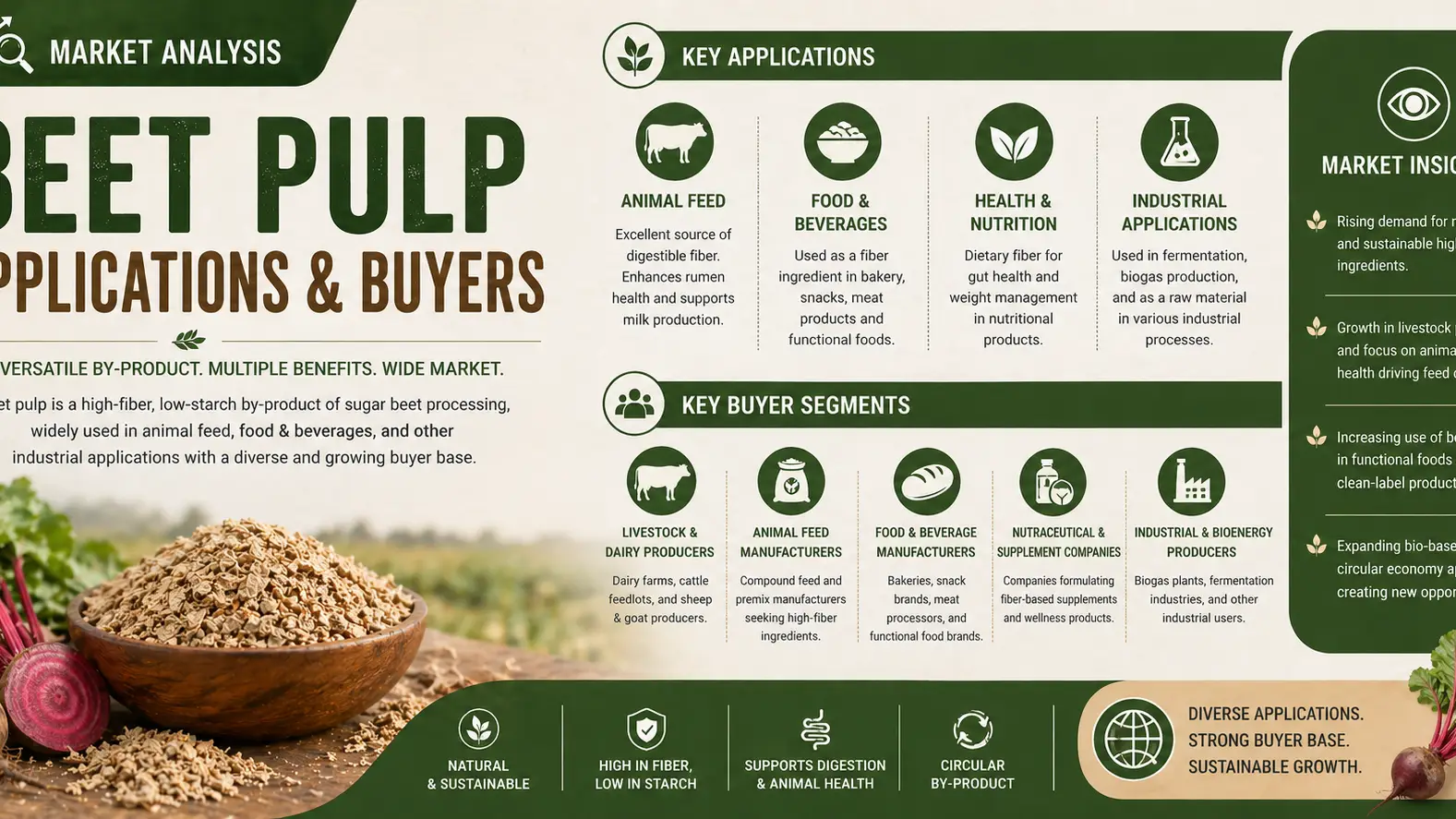

In 2026, beet pulp continues to strengthen its position as a key platform ingredient within the global feed and agri-processing ecosystem. Derived from sugar beet extraction, it supports sustainable livestock nutrition with strong fiber digestibility. The market expands at a 4.8% CAGR, driven by demand for cost-efficient feed alternatives. Average global pricing ranges between USD 160–240/MT, while production volumes reach nearly 25 million MT (dry equivalent), reflecting its established role in circular agricultural value chains.

Beet pulp is widely used in ruminant diets as a digestible fiber source replacing grains in dairy and beef feed formulations. Feed manufacturers incorporate it into compound and pelleted feeds to enhance rumen efficiency and reduce ration costs. Adoption is strongest in intensive livestock systems, accounting for about 38% of total demand, as nutritionists prioritize stable energy release and improved feed conversion efficiency in commercial operations.

Demand is led by dairy cooperatives, feed mills, and large cattle integrators across Europe, North America, and the Middle East. These buyers use beet pulp to offset grain price volatility and stabilize milk yields. Long-term contracts dominate procurement strategies, ensuring supply security. In premium dairy operations, inclusion rates have increased by 12–18%, highlighting its growing role as a strategic feed substitute in high-performance livestock systems.

Beet pulp prices in 2026 track sugar beet harvest cycles and EU processing output. Export ranges sit between USD 160–240/MT, with dehydrated grades commanding higher premiums. Freight costs and energy pricing add short-term volatility, especially in Asia-bound shipments. However, integrated supply agreements with sugar processors help stabilize baseline pricing and reduce extreme fluctuations across global trade corridors.

European Union accounts for nearly 45% of global beet pulp output, followed by Russia and the United States, with rising contributions from Turkey and China. Total production is close to 25 million MT annually (dry equivalent). Processors continue improving extraction efficiency and drying capacity, enabling year-round exports and strengthening supply chain resilience against seasonal agricultural variability.

In summary, beet pulp reinforces its role as a platform feed ingredient within integrated agri-processing systems, bridging sugar production and livestock nutrition markets. As demand for efficient, circular inputs grows, its strategic importance is expected to deepen. For global buyers seeking consistent sourcing, Tradeasia International offers value-added supply chain solutions and reliable distribution networks across key regions, supporting long-term procurement stability in an increasingly competitive feed ingredients market.

Sources

https://www.oecd.org/en/publications/oecd-fao-agricultural-outlook-2021-2030_19428846-en.html

https://www.sciencedirect.com/science/article/pii/S0960852421019222

https://www.usdanalytics.com/industry-reports/beet-pulp-market

We're committed to your privacy. Tradeasia uses the information you provide to us to contact you about our relevant content, products, and services. For more information, check out our privacy policy.

English

English

Indonesian

Indonesian

简体字

简体字

العربية

العربية

Español

Español

Français

Français

Português

Português

日本語

日本語

한국어

한국어

Tiếng Việt

Tiếng Việt