Explore our network of country and industry based websites to access localized information, product offerings, and business services across our group.

Log in to start sending quotation requests for any product.

Don't have an account? Sign Up Here

Home Canola Meal Market 2026: Applications, Buyers & Global Demand Dynamics

Trade Insights | Applications and Buyers | 28 April 2026

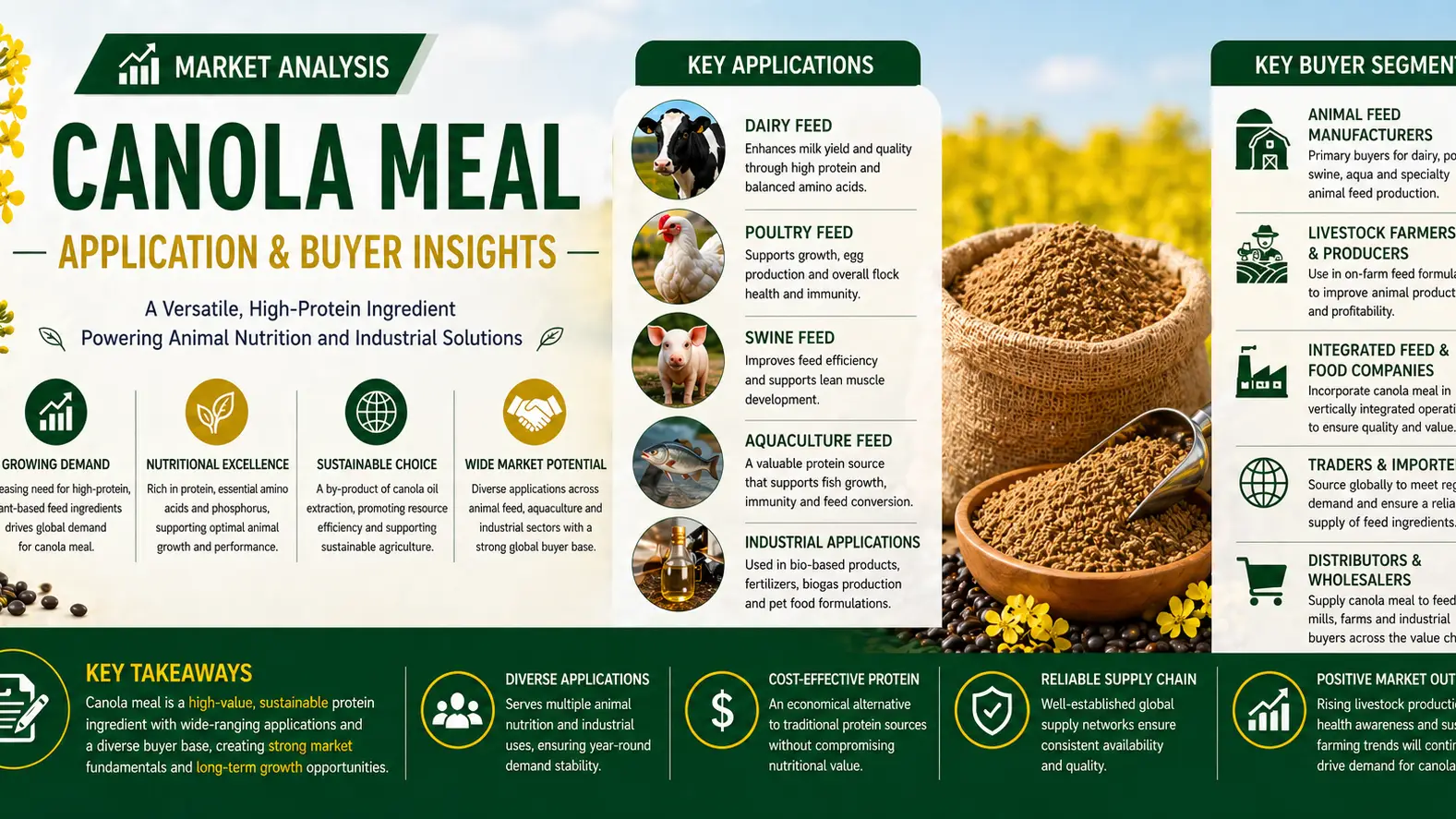

In 2026, the canola meal market continues to strengthen its position as a critical plant-based protein source in global animal nutrition systems. Derived as a by-product of canola oil extraction, canola meal offers a high-protein, cost-effective feed ingredient widely used across livestock sectors. With global production reaching approximately 68 million metric tons, the market is expanding steadily at a CAGR of 4.8%, driven by rising demand for sustainable and alternative protein feed ingredients. Positioned as a key agricultural input, canola meal increasingly functions as a strategic platform ingredient within the broader feed and agri-commodity ecosystem.

Canola meal is primarily utilized in poultry, swine, and dairy feed formulations due to its balanced amino acid profile and digestibility. In 2026, poultry feed alone accounts for nearly 42% of total consumption, as producers seek alternatives to soybean meal amid volatile pricing. Its application in ruminant diets is also expanding, particularly in North America and Europe, where nutrition efficiency is prioritized. The growing integration of canola meal into aquafeed formulations further diversifies its demand base.

The buyer landscape is dominated by large-scale feed manufacturers, integrated livestock producers, and aquaculture feed companies. Commercial feed mills in China, the United States, and the European Union represent the largest procurement hubs. Meanwhile, independent livestock farms in emerging economies increasingly participate in spot purchasing due to fluctuating feed grain costs. These buyers are collectively responding to price competitiveness, with canola meal averaging USD 250–350/MT depending on protein content and region.

Canada remains the largest exporter, supported by strong crushing capacity, while Australia and the EU maintain significant regional supply roles. Global trade flows are shaped by logistics efficiency and protein meal substitution trends. The supply chain remains tightly linked to rapeseed harvest cycles, with seasonal volatility influencing availability and pricing. Export-oriented crushing facilities are increasingly optimizing output to stabilize global distribution networks.

Pricing in 2026 reflects a complex interplay of oilseed availability, energy costs, and feed demand cycles. Trade tensions and freight fluctuations have added volatility, although long-term contracts help stabilize procurement for large buyers. With tightening global protein meal supply, canola meal continues to gain competitiveness against soybean meal, reinforcing its role in diversified feed strategies.

As a versatile and protein-rich feed ingredient, canola meal is firmly positioned within global agricultural supply chains, evolving beyond a by-product into a strategic feed commodity. Its role as a canola meal platform ingredient in animal nutrition underscores its long-term relevance in sustainable protein systems. Looking ahead, partnerships and efficient sourcing will define competitive advantage across the value chain.

Sources

https://www.fas.usda.gov/data/oilseeds-world-markets-and-trade

https://www.oecd.org/agriculture/oecd-fao-agricultural-outlook/

We're committed to your privacy. Tradeasia uses the information you provide to us to contact you about our relevant content, products, and services. For more information, check out our privacy policy.

English

English

Indonesian

Indonesian

简体字

简体字

العربية

العربية

Español

Español

Français

Français

Português

Português

日本語

日本語

한국어

한국어

Tiếng Việt

Tiếng Việt